Why Tokenization Fails at Scale Without Compliance-Native Infrastructure

Tokenization has proven that real-world assets can be issued on-chain.

What it has not yet proven is that those assets can be operated at institutional scale.

Most tokenization initiatives fail not because issuance is difficult, but because compliance is treated as a feature that can be added later. In regulated markets, this assumption does not hold.

Compliance is not an optional layer. It defines who can interact with an asset, under what conditions, across jurisdictions, and throughout its lifecycle. When compliance is bolted on after issuance, enforcement fragments, operational risk compounds, and regulatory confidence erodes.

As institutions move from pilot programs to production deployments, the distinction between platform-level complianceand compliance-native infrastructure becomes decisive.

This guide explains why compliance retrofitting fails, how institutions evaluate regulatory risk, and what it takes to build tokenized markets that can survive real-world conditions at scale.

INDEX (TABLE OF CONTENTS)

- What “Compliance Is Not a Feature” Actually Means

Understanding compliance as a structural requirement, not a capability - Why Compliance Retrofitting Fails at Scale

Regulatory fragmentation, operational risk, and compliance drift - How Institutions Evaluate Compliance Risk

What serious buyers look for before committing capital - Compliance as Infrastructure: The Correct Model

Embedding regulatory logic at the asset level - Asset-Level vs Platform-Level Compliance

Why enforcement location determines survivability - Why Compliance-Native Systems Scale

Operating under regulatory pressure and market stress - Common Misconceptions About Compliance in Tokenization

Where most narratives break down - Where Zoniqx Fits

Implementing compliance-native infrastructure in practice - What This Means for the Future of Tokenized Markets

How the market will consolidate around trusted infrastructure - Key Takeaways

What institutions, builders, and regulators should internalize

1. What “Compliance Is Not a Feature” Actually Means

In many tokenization systems, compliance is treated as a capability that can be added after an asset is issued. This often takes the form of integrations with identity providers, manual approval workflows, or platform-level restrictions applied at the point of transaction.

In regulated markets, this framing is incorrect.

Compliance does not enhance an asset. It defines it.

Compliance determines:

- Who is legally permitted to hold the asset

- Who may transfer it and under what conditions

- How ownership limits are enforced

- What reporting and disclosure obligations apply

- How positions are restricted, frozen, or unwound during regulatory or market stress

These controls are not optional. They are the rules under which the asset is allowed to exist and operate.

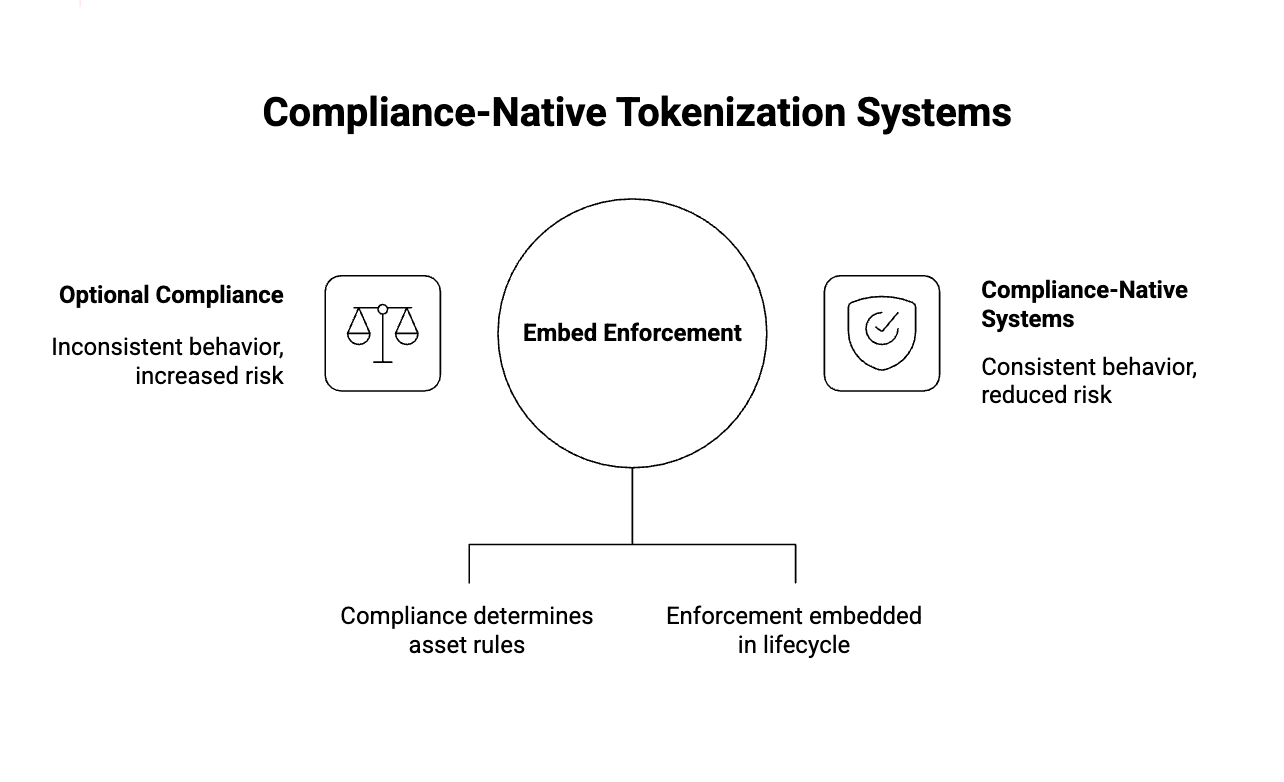

When compliance is treated as a feature, it becomes optional by design. Optional enforcement may appear sufficient at issuance, but it does not survive scale. As assets move across venues, jurisdictions, and participants, feature-based compliance fragments, creating inconsistent behavior and increasing regulatory and operational risk.

In contrast, compliance-native systems embed enforcement directly into the asset lifecycle. The asset behaves consistently regardless of where it is issued, traded, or settled because the rules governing it are inseparable from the asset itself.

This distinction becomes decisive as tokenization moves from experimentation to institutional deployment. At scale, compliance is not something added to an asset. It is the structure that governs how the asset functions in the real world.

2. Why Compliance Retrofitting Fails at Scale

Compliance retrofitting refers to the practice of adding regulatory controls to a tokenized asset after issuance, typically through platform-level restrictions, off-chain procedures, or manual oversight.

While this approach may appear workable in early pilots, it breaks down as assets begin operating across jurisdictions, venues, and market participants.

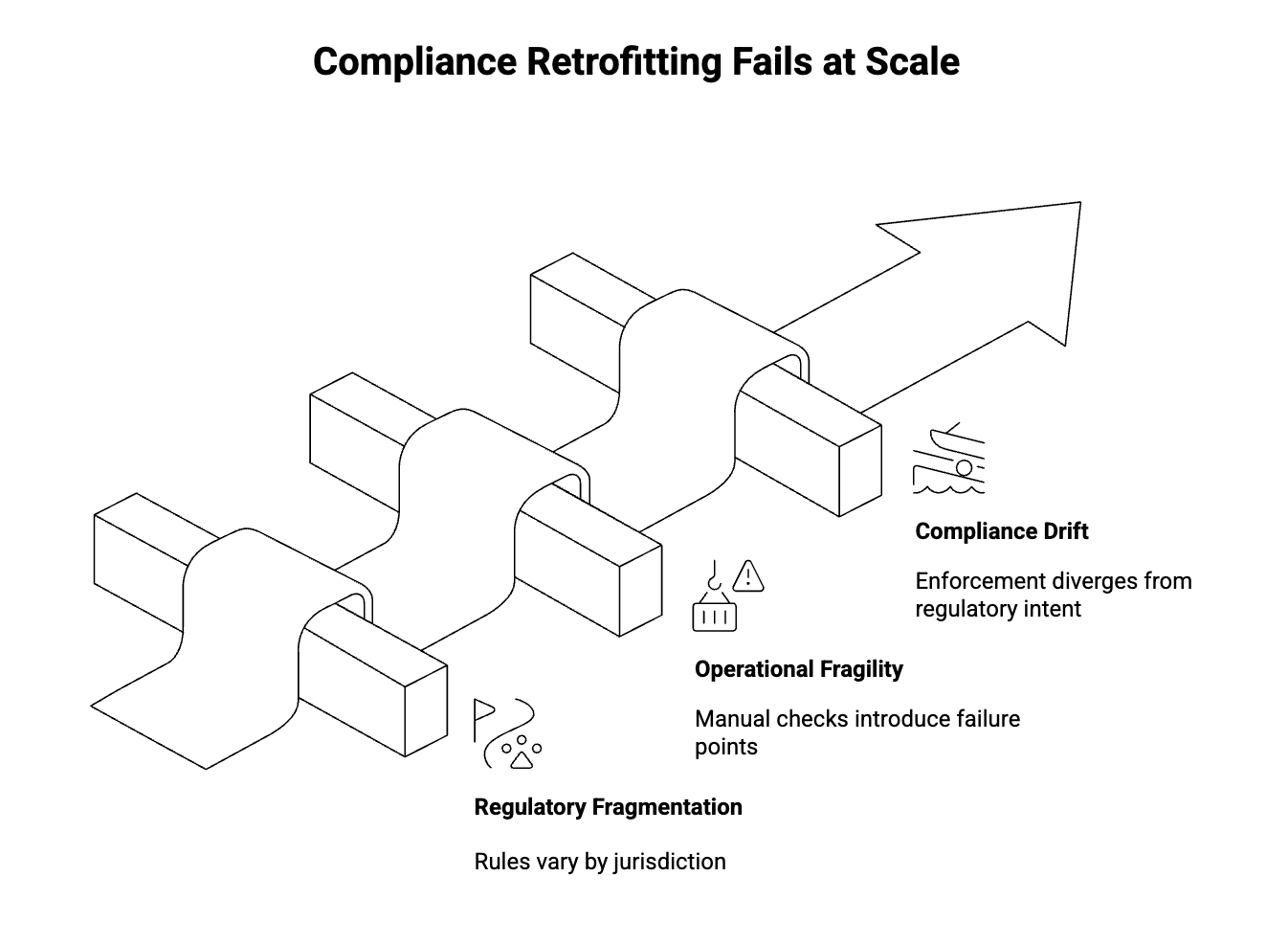

Regulatory Fragmentation

Regulatory requirements are not uniform. Different jurisdictions impose distinct rules around investor eligibility, transferability, holding limits, reporting obligations, and settlement constraints.

When compliance is retrofitted, each venue or intermediary implements these rules independently. As a result, the same asset can behave differently depending on where and how it is traded. This inconsistency introduces regulatory ambiguity and increases exposure for issuers and operators.

Institutions cannot scale systems where regulatory enforcement varies by venue.

Operational Fragility

Retrofit compliance models often depend on manual checks, centralized approvals, or off-chain reconciliation processes. These controls introduce points of failure that become increasingly difficult to manage as transaction volume grows.

Under real-world conditions—secondary market activity, cross-border participation, or market stress—manual enforcement does not scale. Delays, errors, and inconsistencies become systemic risks rather than edge cases.

Institutions design for enforcement that operates automatically and predictably. Retrofitted systems do not meet this standard.

Compliance Drift

Over time, tokenized assets interact with new venues, new participants, and evolving regulatory frameworks. When compliance logic is not embedded directly into the asset lifecycle, enforcement gradually diverges from regulatory intent.

This drift is often incremental and difficult to detect until it becomes material. Correcting it after the fact requires costly remediation, legal intervention, or asset-level intervention, all of which undermine confidence.

At scale, compliance drift is not an anomaly. It is a structural outcome of retrofit architectures.

3. How Institutions Evaluate Compliance Risk

Institutions do not evaluate compliance as a point-in-time status or a checklist to be completed at issuance.

They evaluate whether compliance can be sustained, proven, and enforced over the full lifecycle of an asset.

When assessing tokenized assets and the infrastructure that supports them, institutions focus on a small number of fundamental questions:

- Can regulatory rules be enforced consistently over time, not just at launch?

- Can compliance be demonstrated programmatically during audits or regulatory reviews?

- Can the asset operate across jurisdictions without creating conflicting obligations?

- Can positions be restricted, frozen, or unwound cleanly under stress scenarios?

- Can enforcement operate without continuous manual intervention?

If any of these conditions are unclear, institutions slow adoption or limit exposure regardless of how innovative the technology may be.

This evaluation reflects how risk is managed in traditional financial markets. Institutions assume that regulations will evolve, transaction volumes will increase, and edge cases will become routine. Systems are therefore judged on their ability to maintain compliance under pressure, not on their performance during ideal conditions.

For this reason, institutions favor infrastructure that treats compliance as a continuous operating requirement rather than a transactional control. Predictability, auditability, and repeatable enforcement are valued more highly than speed or flexibility at launch.

At scale, compliance is not assessed by intent or design claims. It is assessed by whether enforcement can be trusted when conditions change.

4. Compliance as Infrastructure

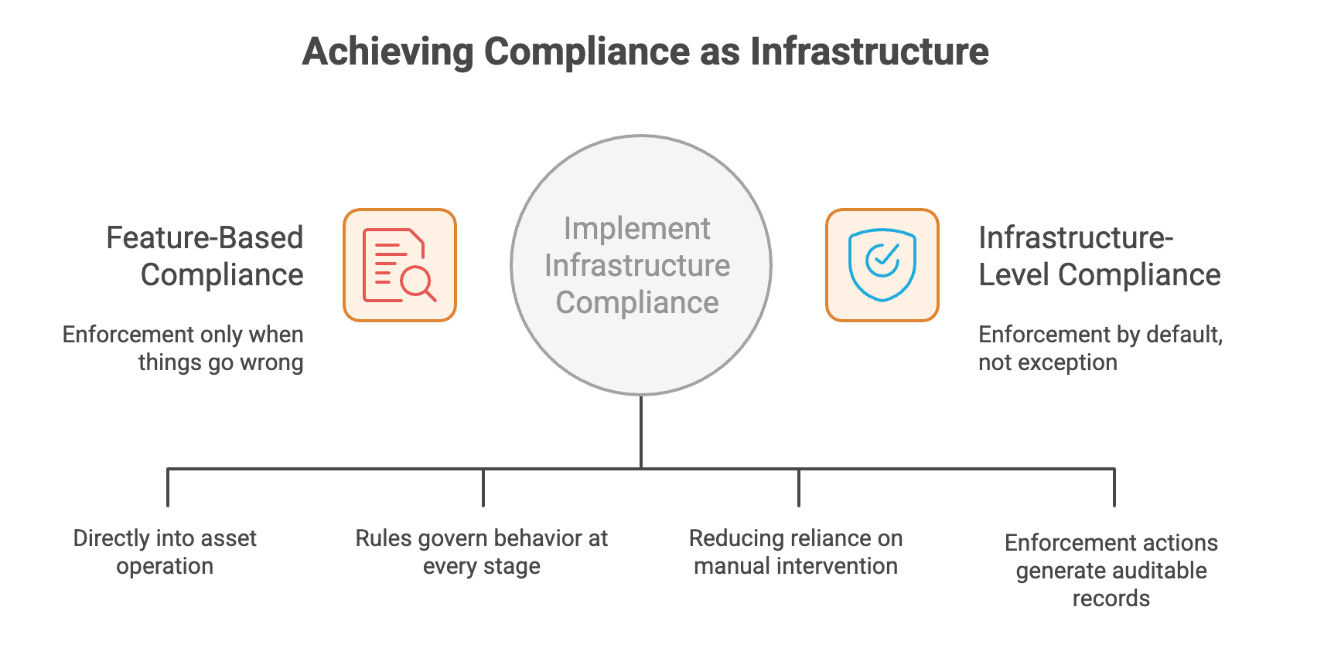

In regulated markets, systems that scale are built around enforcement, not exceptions.

Compliance as infrastructure means that regulatory logic is embedded directly into the operation of an asset, rather than applied externally through platforms, processes, or manual controls.

In a compliance-native model, enforcement is continuous. Rules are not checked at specific moments; they govern behavior at every stage of the asset lifecycle. This includes issuance, holding, transfer, settlement, reporting, and, when required, restriction or unwind.

Infrastructure-level compliance exhibits several defining characteristics:

- Persistence: Regulatory rules remain attached to the asset regardless of where it operates or who interacts with it.

- Consistency: The asset behaves predictably across venues and jurisdictions because enforcement is not re-implemented at each point of interaction.

- Automation: Compliance is enforced programmatically, reducing reliance on manual intervention and discretionary controls.

- Auditability: Enforcement actions and state changes generate verifiable records that can be examined after the fact.

When compliance functions as infrastructure, it becomes largely invisible during normal operation. Its presence is felt primarily through the absence of failures, exceptions, or remediation events. This is the same property that defines other forms of financial infrastructure, such as clearing, settlement, and custody systems.

By contrast, systems that treat compliance as a feature tend to surface enforcement only when something goes wrong. At scale, this approach increases operational friction, regulatory exposure, and uncertainty.

As tokenized markets mature, the distinction between feature-based compliance and infrastructure-level compliance becomes increasingly material. Infrastructure survives scrutiny because it is designed to enforce rules by default, not by exception.

At institutional scale, compliance does not sit alongside the system. It is the system.

5. Asset-Level vs Platform-Level Compliance

Where compliance is enforced matters as much as how it is enforced.

In tokenized systems, regulatory controls are typically applied at one of two levels: the platform or the asset itself. The difference between these approaches becomes decisive as assets scale across venues and jurisdictions.

Platform-Level Compliance

In platform-level models, compliance rules are enforced by the application or venue facilitating issuance or trading. Each platform interprets and implements regulatory requirements independently.

This approach results in:

- Different enforcement logic across venues

- Repeated re-implementation of the same regulatory rules

- Assets behaving differently depending on where they are traded

- Higher operational and compliance overhead

- Limited end-to-end auditability

While platform-level compliance may be sufficient for early-stage pilots, it introduces fragmentation as assets move beyond their original environment.

Asset-Level Compliance

In asset-level models, regulatory rules are embedded directly into the asset lifecycle. Enforcement is inseparable from the asset itself and does not depend on the platform through which it is accessed.

This approach enables:

- A single rulebook governing asset behavior

- Consistent enforcement across markets and jurisdictions

- Reduced operational complexity

- Predictable behavior under regulatory scrutiny

- Audit-ready records by design

Asset-level compliance aligns with how institutions manage risk in traditional markets, where controls are attached to the instrument rather than the venue.

As tokenized assets begin to trade across multiple platforms and means of access, asset-level enforcement becomes a requirement rather than an architectural preference.

At scale, institutions do not rely on platforms to remain compliant. They rely on assets that cannot behave otherwise.

6. Why Compliance-Native Systems Scale

Scaling tokenization is not a function of issuing more assets. It is a function of operating assets under real-world constraints.

As transaction volumes increase and assets move across jurisdictions, markets, and participants, systems are exposed to regulatory pressure, operational stress, and edge cases that are not visible in early pilots. The ability to withstand these conditions determines whether a system can scale.

Compliance-native systems are designed with these pressures in mind.

By embedding regulatory enforcement directly into the asset lifecycle, compliance-native architectures ensure that rules are applied consistently as complexity increases. Enforcement does not degrade as volume grows, and regulatory intent is preserved across new venues and use cases.

This approach produces several scaling advantages:

- Predictable behavior: Assets behave consistently regardless of where or how they are accessed, reducing uncertainty for issuers and participants.

- Operational resilience: Automated enforcement reduces dependency on manual controls that fail under load.

- Regulatory durability: Systems can accommodate regulatory change without requiring asset-level remediation or venue-by-venue reconfiguration.

- Market confidence: Participants can engage at scale knowing that compliance is enforced by design rather than by oversight.

By contrast, systems optimized for speed or flexibility at launch often encounter friction as they scale. Manual processes multiply, exceptions increase, and regulatory exposure accumulates. Growth slows not because demand is absent, but because risk becomes difficult to manage.

In mature financial markets, scale is achieved through infrastructure that absorbs complexity rather than amplifies it. Compliance-native systems follow the same principle.

At institutional scale, survivability is determined not by how quickly assets can be issued, but by how reliably they can be operated.

7. Common Misconceptions About Compliance in Tokenization

As tokenization gains traction, several recurring assumptions continue to shape how compliance is approached. While these assumptions may appear reasonable in early-stage environments, they do not hold under institutional scrutiny or real-world operating conditions.

“Compliance Slows Innovation”

This assumption confuses enforcement with friction.

In regulated markets, uncertainty is what slows innovation. When rules are unclear, inconsistently applied, or subject to manual interpretation, institutions delay adoption and limit exposure.

Clear, enforceable compliance frameworks enable innovation by providing predictability. They allow institutions to design products, workflows, and markets with confidence that regulatory requirements will be met consistently.

Innovation accelerates when enforcement is reliable, not when it is optional.

“Compliance Can Be Added Once There Is Demand”

Institutional demand does not precede compliance. It depends on it.

Institutions require confidence that regulatory requirements will be enforced before they commit capital, integrate systems, or engage secondary markets. Adding compliance after issuance often requires restructuring assets, modifying contracts, or limiting distribution, all of which increase risk and cost.

Systems that defer compliance typically stall at the point where scale would otherwise begin.

“Custom Compliance Per Platform Is Flexible”

Custom enforcement across platforms is often mistaken for flexibility.

In practice, fragmented compliance logic creates:

- Inconsistent asset behavior

- Increased operational overhead

- Higher audit and reconciliation costs

- Greater exposure to regulatory misalignment

Institutions favor standardization over customization when it comes to enforcement. Flexibility is achieved through jurisdiction-aware rules applied consistently, not through bespoke implementations at each venue.

“Compliance Is a Legal Problem, Not a Technical One”

Compliance is a legal requirement, but enforcement is a technical responsibility.

Relying solely on policies, procedures, or contractual terms without embedding enforcement into system architecture introduces execution risk. Institutions increasingly expect compliance to be supported by technical controls that reduce reliance on manual oversight.

At scale, enforcement must be executable by systems, not just documented by teams.

These misconceptions persist because they are rarely tested under real operating conditions. As tokenized markets mature, the gap between assumption and reality becomes increasingly visible.

Systems that treat compliance as foundational adapt.

Systems that treat it as optional eventually stall.

8. Zoniqx as Compliance-Native Infrastructure

Zoniqx is designed to implement compliance as infrastructure by embedding regulatory enforcement directly into the asset lifecycle, rather than relying on platform-level controls or post-issuance processes.

At the core of this approach is zCompliance, the enforcement layer responsible for ensuring that regulatory rules are applied consistently, continuously, and programmatically as assets operate across markets and jurisdictions.

Zoniqx does not treat compliance as a workflow.

It treats compliance as a system property.

zCompliance: Asset-Level Enforcement by Design

zCompliance functions as the regulatory enforcement engine within the Zoniqx infrastructure stack. Its role is not to validate compliance at isolated moments, but to govern asset behavior throughout its lifecycle.

zCompliance embeds regulatory logic directly into the asset, ensuring that enforcement is inseparable from the asset itself.

This enables:

- Continuous enforcement

Regulatory rules are applied at issuance, holding, transfer, settlement, and reporting, without reliance on manual checks or venue-specific overrides. - Jurisdiction-aware logic

Assets can operate across jurisdictions while respecting differing regulatory requirements through structured, rule-based enforcement rather than fragmented customization. - Consistent behavior across venues

Because enforcement is asset-level, the same asset behaves predictably regardless of where it is accessed or traded. - Reduced operational risk

Programmatic enforcement minimizes reliance on human intervention, lowering the likelihood of error, delay, or inconsistent application of rules.

Preventing Compliance Drift at Scale

One of the primary failure modes in tokenized markets is compliance drift, where enforcement gradually diverges from regulatory intent as assets scale across venues, participants, and regulatory changes.

zCompliance is designed to prevent this outcome by:

- Ensuring regulatory rules persist with the asset

- Maintaining enforcement consistency as assets move across environments

- Supporting updates to regulatory logic without requiring asset-level remediation

- Generating verifiable records of enforcement actions over time

This allows institutions to demonstrate not only that compliance exists, but that it has been maintained continuously under real operating conditions.

Compliance Beyond Issuance

Most tokenization systems concentrate enforcement at issuance and rely on external controls once assets enter secondary markets.

zCompliance is designed for post-issuance reality.

It ensures that:

- Transfer restrictions remain intact in secondary trading

- Eligibility requirements continue to be enforced

- Reporting obligations persist as ownership changes

- Assets can be restricted or unwound cleanly when required

This focus on post-issuance enforcement aligns with how institutions assess risk and regulatory exposure.

Infrastructure, Not a Platform

Zoniqx integrates with existing institutional systems rather than replacing them. zCompliance operates as an enforcement layer that coordinates identity, permissions, and regulatory logic across issuance, trading, and settlement environments.

This allows institutions to move assets on-chain while preserving established operating models, compliance frameworks, and risk controls.

By treating compliance as a foundational system property, Zoniqx enables tokenized markets to operate predictably under regulatory scrutiny.

As tokenization moves from experimentation to production, enforcement by design becomes a prerequisite rather than a differentiator.

Zoniqx, through zCompliance, exists to meet that requirement.

9. What This Means for the Future of Tokenized Markets

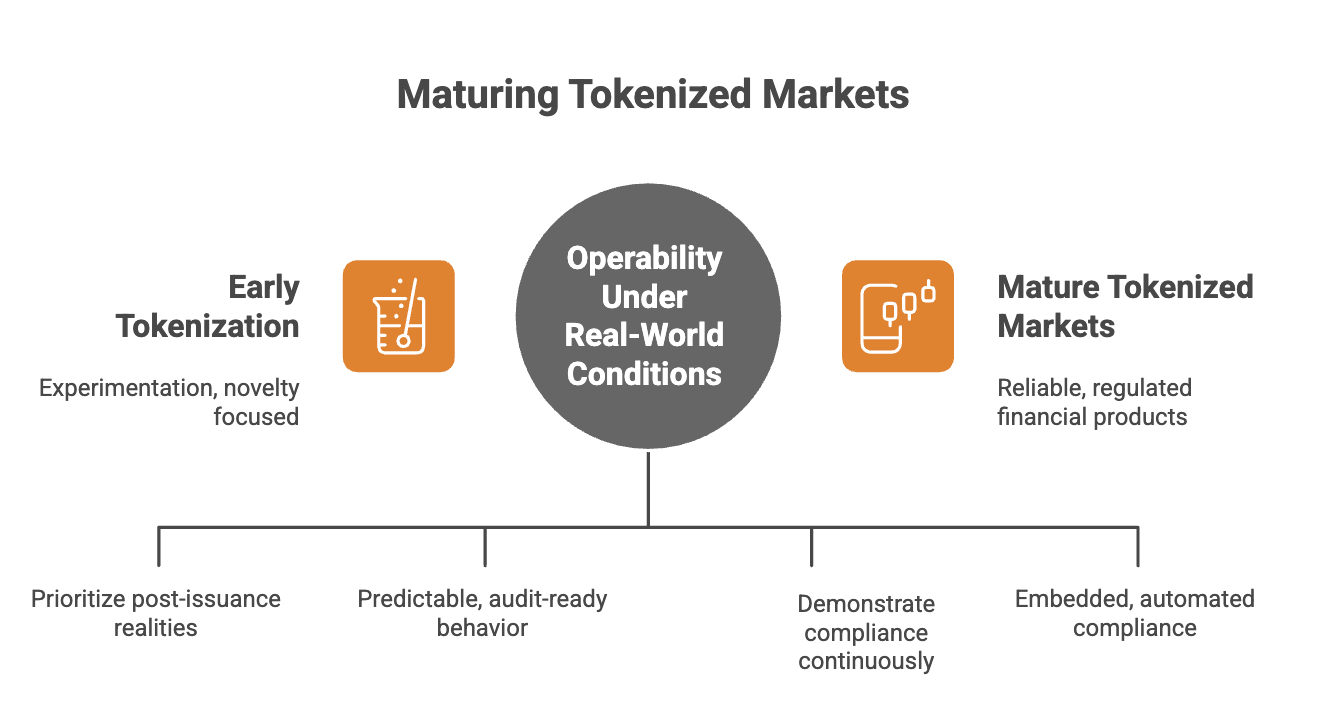

As tokenized markets mature, the criteria for success are changing.

Early phases of tokenization were defined by experimentation. The primary question was whether real-world assets could be issued on-chain at all. That question has largely been answered.

The next phase is defined by operability under real-world conditions.

Regulators, institutions, and market operators are no longer evaluating tokenization based on novelty or proof of concept. They are evaluating whether systems can enforce rules consistently, withstand regulatory scrutiny, and operate reliably as assets scale across jurisdictions and venues.

This shift has several implications for the future of tokenized markets.

First, enforcement will matter more than issuance. Systems that focus on launch mechanics without addressing post-issuance realities will struggle to move beyond pilot deployments.

Second, standardization will follow infrastructure, not platforms. Markets will consolidate around systems that provide predictable, audit-ready behavior rather than bespoke implementations that vary by venue.

Third, regulatory confidence will become a competitive advantage. Institutions will gravitate toward infrastructure that allows them to demonstrate compliance continuously, not defensively after the fact.

Finally, tokenization will increasingly resemble traditional market infrastructure. As enforcement becomes embedded and automated, tokenized assets will behave less like experimental instruments and more like regulated financial products operating on modern rails.

The future of tokenized markets will not be defined by who moved first.

It will be defined by which systems can operate reliably when conditions are complex, volumes are high, and scrutiny is unavoidable.

In that environment, compliance is no longer a constraint on growth.

It is the condition that makes sustainable growth possible.

10. Key Takeaways (FAQ)

What does “compliance is not a feature” mean in tokenization?

It means compliance is not an optional capability added after issuance.

In regulated markets, compliance defines how an asset is allowed to exist, operate, and change ownership across its entire lifecycle.

When treated as a feature, compliance becomes inconsistent and fragile at scale.

Why does compliance retrofitting fail in tokenized markets?

Compliance retrofitting fails because enforcement is applied unevenly across venues, jurisdictions, and lifecycle stages. Over time, this leads to regulatory fragmentation, operational risk, and compliance drift.

At institutional scale, optional or manual enforcement does not survive.

How do institutions evaluate compliance in tokenization?

Institutions evaluate whether compliance can be enforced continuously, proven during audits, maintained across jurisdictions, and operated without manual intervention.

They assess survivability under stress, not compliance at launch.

What is compliance-native infrastructure?

Compliance-native infrastructure embeds regulatory enforcement directly into the asset lifecycle. Rules are enforced programmatically and persist regardless of where the asset is issued, traded, or settled.

Compliance becomes a system property rather than a workflow.

Why is asset-level compliance preferred over platform-level compliance?

Asset-level compliance ensures that a single rulebook governs asset behavior everywhere. Platform-level compliance requires repeated enforcement and leads to inconsistent behavior across venues.

Institutions prefer controls attached to the asset, not the platform.

Does compliance slow down tokenization?

No. Uncertainty slows tokenization.

Clear, enforceable compliance frameworks enable institutions to scale participation confidently. Predictability accelerates adoption more effectively than speed at issuance.

Can compliance be added later once demand exists?

Institutional demand depends on compliance being enforced from the start. Adding compliance later often requires restructuring assets, limiting distribution, or remediating risk, all of which slow adoption.

How does Zoniqx address compliance at scale?

Zoniqx implements compliance as infrastructure by embedding enforcement directly into the asset lifecycle through its compliance-native architecture.

At the core of this approach is zCompliance, which ensures regulatory rules are applied continuously, consistently, and across jurisdictions as assets operate at scale.

Why does compliance matter more as tokenization matures?

As tokenized markets move from pilots to production, regulators and institutions focus on enforcement, auditability, and operational reliability.

Systems that cannot demonstrate compliance under pressure will struggle to scale.

What ultimately determines success in tokenized markets?

Success is determined by whether assets can operate reliably under real-world conditions. Issuance proves feasibility. Compliance-native infrastructure determines survivability.

Final takeaway

Tokenization does not fail because assets cannot be issued.

It fails when compliance cannot scale.

Markets will consolidate around infrastructure that enforces compliance by design, not by exception.

About Zoniqx

Zoniqx is a Silicon Valley–headquartered fintech company building the operating system and distribution rails for tokenized real-world assets (RWAs). The operating system governs how assets behave and how they reach markets, across institutions, jurisdictions, and infrastructures, without becoming a marketplace or custodian.

Its modular product suite, including z360, zCompliance, zPayRails, zConnect, zIdentity, zInsights, zIndex, and zProtocol built on DyCIST (ERC-7518), provides an interoperable, compliant, and chain-agnostic infrastructure layer supporting tokenization across public, private, and hybrid blockchains, and delivered through enterprise-grade SDKs and APIs.

Zoniqx is the neutral control layer that embeds policy, identity, and compliance into the asset itself and enables compliant distribution at network scale, so tokenized markets can operate consistently and safely everywhere.

If you are a financial institution, issuer, or platform looking to integrate tokenization into existing regulated workflows, without assuming custody, liquidity, or intermediary risk, visit www.zoniqx.com/contact to explore partnerships or tokenization initiatives with Zoniqx.

Disclaimer

This article is for informational purposes only and does not constitute legal, financial, or regulatory advice. References to SEC are based on public statements and do not imply endorsement or legal interpretation. Readers are encouraged to consult with legal or regulatory professionals before engaging in asset tokenization. Zoniqx operates in full compliance with applicable laws and supports regulatory clarity in the tokenization ecosystem.

%20Part%201.jpg)